When your car is totaled in an accident, your insurance payout depends on how the company calculates your vehicle’s value. This article breaks down the difference between ACV vs Replacement Cost in total loss settlements—two methods that can lead to very different outcomes.

The two main approaches are:

- Actual Cash Value (ACV)

- Replacement Cost Coverage

These terms determine how much you’ll get paid—and the difference can be thousands of dollars.

In this article, you’ll learn:

- What ACV and Replacement Cost actually mean

- How they affect your total loss settlement

- Real examples of how payouts change

- When it’s worth upgrading your policy

By the end, you’ll understand which payout type fits you best and how to avoid being underpaid after a total loss.

What Is ACV and Replacement Cost: How Does It Work?

What Is ACV?

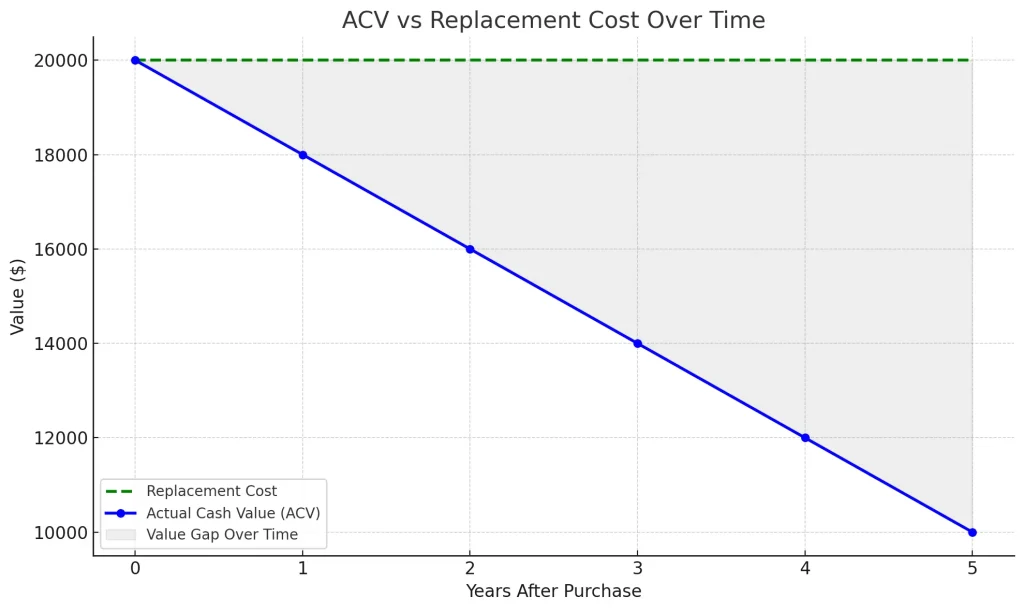

Actual Cash Value (ACV) is the most common way insurers calculate a payout. It’s based on what your car was worth right before the accident—not when you bought it.

- How Insurance Companies Calculate ACV

The ACV formula is simple:

ACV = Replacement Cost – Depreciation

Let’s say your car would cost $25,000 new. But it’s 5 years old and has 80,000 miles. The insurer subtracts the loss in value (say, $9,000), and you get $16,000 before your deductible. - Common Depreciation Factors:

- Vehicle age

- Mileage

- Prior damage or repairs

- Wear and tear

- Market resale trends in your area

This is why most total loss checks feel lower than expected.

What Is Replacement Cost?

Replacement Cost Coverage gives you the amount needed to buy a new or similar car, without subtracting for age or wear.

It’s like hitting reset on your vehicle’s value. But here’s the catch: this type of coverage is optional and costs more.

When Is Replacement Coverage Offered?

Not every insurer offers it, and it’s usually limited to:

- New cars (less than 1–2 years old)

- Leased or financed vehicles

- Customers who pay extra for upgraded coverage

Key Differences Between ACV and Replacement Cost

| Feature | Actual Cash Value (ACV) | Replacement Cost |

|---|---|---|

| Deducts depreciation? | Yes | No |

| Pays market value? | Yes | No (pays full value) |

| Costs more to insure? | No | Yes |

| Common in standard policy | Yes | No (add-on) |

| Higher payout? | Usually lower | Usually higher |

Bottom line: ACV is cheaper up front, but can leave you with less money when you need it most.

Why This Matters in a Total Loss Settlement

When your car is totaled, your insurer decides what they owe you based on your policy type. That choice affects:

- How much you can afford for your next car

- Whether you’ll need to take out a loan

- If you’ll come up short replacing your vehicle

If you have ACV, you may get an offer that doesn’t cover a new car. With replacement cost, you’re more likely to walk away whole.

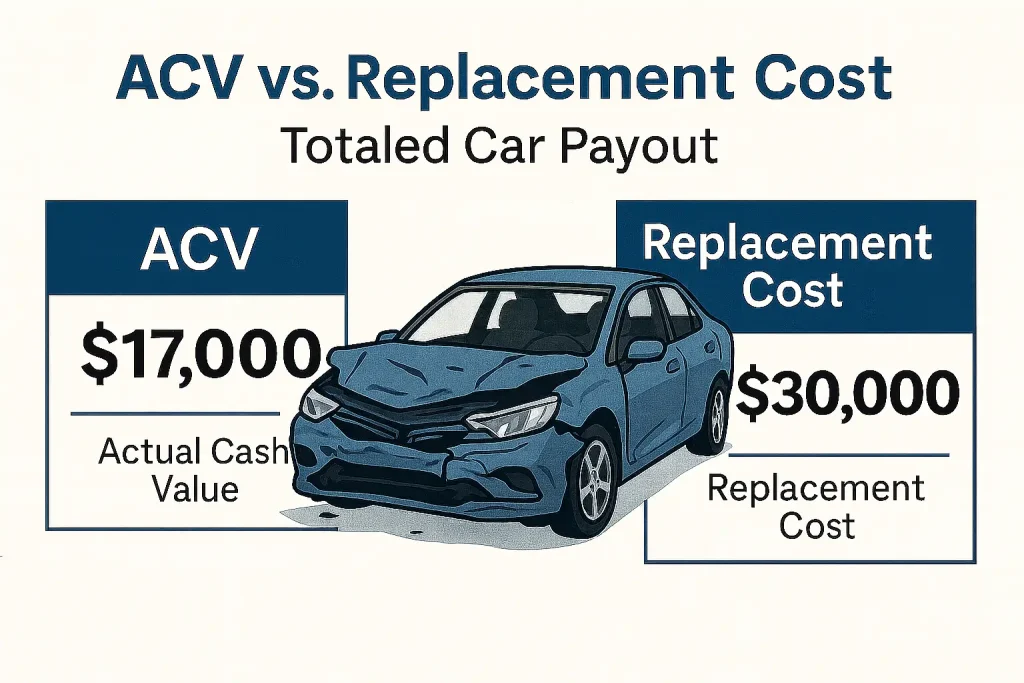

Example: ACV vs Replacement Cost in Action

Scenario:

You buy a car in 2021 for $30,000. In 2025, it’s totaled.

- ACV policy: Value has dropped to $17,000

- Replacement policy: Still pays around $30,000

That’s a $13,000 difference—just based on your policy type.

Is Replacement Cost Coverage Worth It?

It depends on your needs. Consider replacement coverage if:

- You drive a brand-new or leased car

- You don’t want to dip into savings for a new car

- You’re worried about rapid depreciation

- You prefer to keep your monthly budget stable

Yes, it costs more. But it can save you thousands later.

Final Thoughts: ACV vs Replacement Cost

Your total loss settlement can change drastically depending on your coverage. Most people have ACV, which deducts for depreciation. That’s why your check may be smaller than expected.

If you want full protection—especially for newer vehicles—replacement cost coverage is a smart upgrade.

Know what your policy says before the accident happens. Ask your insurer if you qualify for replacement coverage and how it affects your payout. A few dollars more each month could mean a much bigger check later.